Mobile payment apps are rushing us into a cashless, card-free, order-in-one-click, and pay-contactless universe. They accelerate and optimize everything: splitting bills, sending remittances, booking trips, managing expenditures. Fintech revamps our ways with money – mobile wallet apps, m-commerce apps, cryptocurrency platforms, peer-to-peer payment apps, and whatnots! One day we can wake up to a COMPLETELY BANKLESS WORLD.

Don’t laugh! It’s already there! The next-gen peer-to-peer payment apps are card-less, cash-less, and bank-less. In the meantime, though, the mobile payment world is a melting pot of business models, UVPs, and technologies.

Ready to go down the rabbit hole of peer-to-peer mobile payment system development? Follow me!

- What is a peer-to-peer payment app, anyway?

- What can a person-to-person payment app do?

- It takes all sorts to make a peer-to-peer money transfer world

- Four business models of P2P payment applications

- Why build a peer-to-peer payment app here and now

- How to be a peer-to-peer payment wizard: 3 success stories

- PayPal: innovator #1 in person-to-person payments

- Alipay: Chinese PayPal… only better

- Airfox: the Robin Hood of emerging economies

- How to get into P2P payment app development

- Foolproof design

- Regulation compliance

- P2P payment app user journey

- P2P payment app features

- Secure networks: Blockchain

What is a peer-to-peer payment app, anyway?

Think along the lines of Western Union (long before mobile), or PayPal. A peer-to-peer (aka person-to-person, P2P) mobile payment system is an application that we use to make electronic money transfers to a friend, relative, contractor, or employee.

P2P money transfer apps have some common characteristics:

- they are designed for personal use between people who know each other well – hence the lower level of transaction protection compared to commercial apps;

- the time of transaction can last from several minutes to several days, depending on the method used;

- funding requirements range across various peer-to-peer-payment apps (bank account, debit/credit card, dedicated in-app account).

What can a person-to-person payment app do?

Peer-to-peer mobile payment apps have seen more uses than you can imagine:

- paying a merchant / landlord on an installment plan;

- paying a taxi cab service (with discounts calculation);

- setting a borrowing limit for a friend / kid and allowing them to withdraw a set amount, a set number of times and/or at set intervals;

- sending and receiving a friend-to-friend borrowing request;

- transferring money on a borrowing request from a friend /relative (with a comment);

- splitting a dinner / utility bill with a friend / partner;

- sending a money transfer as a gift to loved ones;

- sending remittances to family in another country;

- paying for utilities / internet / other services online.

Or you can go outside your circle of friends and across the borders to make an international money transfer – some P2P payment apps are designed for that:

- P2P FX. Peer-to-peer foreign currency exchange bring together users worldwide. They cut out the middlemen – banks and brokers – and save their clients up to 90% on international exchange and transfer fees.

- P2P lending apps. These apps subsidize users in need by giving repayable microloans at a lower interest than banks. They are lucrative to investors looking to monetize their funds.

- P2P cross-border money transfer apps. Peer-to-peer international money transfer apps make remittances less costly. Once deemed insecure, they are possible now via a mobile app due to smart technologies. This is a promising new market.

So if you still visit your local bank to send money to a friend or pay a bill, consider this: technology within the app allows to do that without leaving home, and from a variety of sources too – bank account, credit card, or via a non-bank agent acting as an escrow.

It takes all sorts to make a peer-to-peer money transfer world

Peer-to-peer payment solutions vary by character (airtime transfer & top-ups, money transfers & payments, merchandise & coupons, travel & ticketing), field of application (retail, travel & hospitality, transportation & logistics, energy & utilities, etc.), location (domestic, cross-border), and business model (bank-centric, standalone financial services, social media-centric, mobile OS/device-centric). A winning business model is crucial in money transfer app development. And top players on the market operate by fairly different business models. Let’s have a closer look.

Four business models of P2P payment applications

Companies researching how to create a mobile peer-to-peer payment app will discover the four types of solutions:

- Bank-centric solutions like Dwolla, Zelle, PopMoney, clearXchange. Many banks deploy mobile payment applications or devices to customers and ensure merchants have the required point-of-sale (POS) acceptance capability. These apps draw from and deposit directly into bank accounts instead of a stored currency account. The role of a mobile network operator is to provide Quality of service (QoS) assurance.

- Standalone financial services like PayPal, Venmo, Square Cash, Alipay, M-Pesa, Airfox. Independent service providers (ISPs) can officially mediate since a Financial Services Action Plan was initiated in Lisbon in 2000. They offer online and in-person P2P/C2B payments with or without checking accounts and debit/credit cards. These apps predominantly have a wallet feature which makes it possible for users to store money before offloading in some bank account or sending it over to their peers. The non-bank model proved valuable in some developing countries where people have limited access to banking.

- Social/messaging/web platforms like Facebook Messenger, Snapchat, Kik, WeChat, Square Cash, G Pay Send. Social media payments figured we’re more likely to send frequent payments to people we have regular contact with. So why not arrange a handy service in the same medium – a messaging app? The apps don’t require strong authentication to complete a transaction, removing friction from the process. WhatsApp, with more than a billion users a day, is trialling the instant bank-to-bank transfer service in India, which would allow 200 million users to transfer money while texting.

- Mobile OS / device manufacturers like Apple Pay, Samsung Pay, Android Pay. They only allow for money transfers inside their product ecosystem. ‘Pay’ is rather a default device feature than an app here. This model works best for developed countries where payment infrastructure is already in place and customers feel comfy using it. The services leverage card tokenization and device-based thumbprint authentication for enhanced security and ease of use.

You might think it intimidating to get into the development of something as complex as peer-to-peer payment apps, with so many big players out there. Why even bother? And how is it even possible?

Okay. Let’s breathe in, breathe out, and take one step at a time. First, focus on ‘why’. Next, deal with ‘how’.

Why build a peer-to-peer payment app here and now

Demand

Three out of four Millennials have made online or mobile P2P payments, according to a recent study by the money-transferring mobile app Zelle. Generation X comes in a close second at 69%, and Baby Boomers at 51%. Convenience is cited as a key adoption factor by 68% of P2P mobile payment app users. Admit it, users love sending money with a few taps and swipes. And the timing to get into payment P2P app development is just right since the pocket of opportunity is getting filled with investment gold.

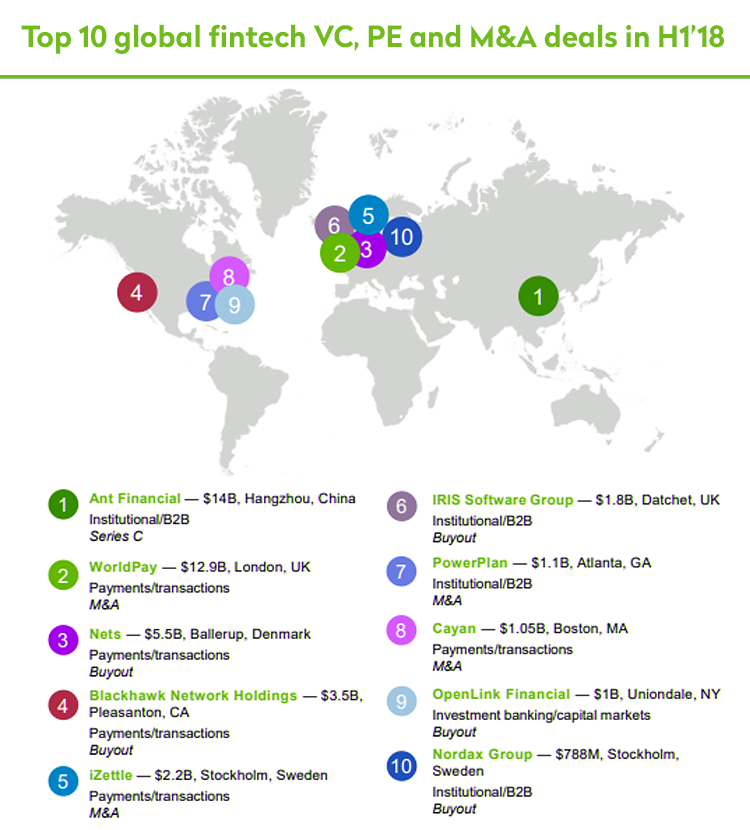

Investment

The mobile P2P payment app market worth is expected to reach $336 billion in 2021. ‘Payments & transactions’ startups have received five out of ten top fintech investments in the first half of this year.

Image source: Pulse in Fintech 2018. Global analysis in investment in fintech, KPMG International (data provided by PitchBook) 9 July, 2018. Data as of 30 June, 2018

Technology

Technological advances allow for new unprecedented models, value-adding to consumers and making businesses more self-reliant.

Alongside more familiar FinTech innovations like NFC and biometrics ID, give a thought to the emerging industry-transforming concepts:

- Real-time payments. RTM enrich the current payment methods with speed, valuable messaging capabilities and immediate availability of transaction status.

- Distributed ledger technology/Blockchain. DLT caters for security and cost-efficiency.

- Conversational interfaces. The expansion of payments to non-physical interfaces may eventually render the traditional UI obsolete. Connected IVAs become smarter and add functionality with the enhancement of NLP and image recognition. Voice-first solutions are about to become a new tech reality.

- Unified platforms. Migrating from a plethora of legacy and pricey systems to one single platform should sweep clean the oversaturated market of payment solutions. Moreover, a single payment experience for customers (based on seamless system interoperability, comparable to mobile telephony) is a more probable future.

Evidently, the financial sector is going through a major digital transformation. Bank and non-bank-centric solutions do not enjoy equal success worldwide. It largely hinges on particular circumstances and leaves us wondering why M-Pesa in Kenya and China’s Alipay took off, while the same model was nowhere near as successful with Paylah! in Singapore and Kakao in South Korea. It’s equally open to debate why some P2P solutions like Snapcash and Venmo shut down while others prosper.

Learn also: How to Create Your Own POS System: Comprehensive Guide for Your Business.

So how to build a mobile payment system that becomes a success? A thorough analysis of use cases might give some insights.

How to be a peer-to-peer payment wizard: 3 success stories

PayPal: innovator #1 in person-to-person payments

PayPal’s co-founder Elon Musk was quick to envisage the potential on the internet to transfer money worldwide. His selectivity in choosing partners for PayPal gained the company its all-time trust. Next, followed some timely acquisitions (VeriSign, Braintree, Venmo, Xoom, Paydiant, Modest), entrance into the online retail market, tie-up with MasterCard. With the inception of PayPal’s new line, Secured Card Service, users could make payments on the websites that did not have PayPal directly but generated a unique MasterCard number on their every checkout. This alone brought a revenue close to $1.8 billion. The number of PayPal’s active registered users has nearly tripled since 2010, showing a 15% year-on-year growth.

Hence, PayPal’s success hinges on several factors:

- stepping into a blue ocean;

- developing a viable business model;

- harnessing network intelligence;

- careful partnerships;

- smart acquisitions;

- timely move into the big time on things like retail POS terminals;

- providing a technology agnostic solution;

- gaining international credibility.

All in all, the company has a huge potential to stay successful over time.

Alipay: Chinese PayPal… only better

Okay, the USA may boast its long-standing PayPal success, but China is already leading the race of peer-to-peer mobile payment apps. Mobile payment transactions in China reached a record 81 trillion yuan (about $12.8 trillion) from January to October last year, dwarfing the estimated $49.3 billion in total mobile payment transactions in the United States last year.

So whatever the claims of China’s copycatting, this time there’s a lesson to learn from the Chinese way of doing business.

Ecosystems of business

Today’s business environments are highly complex and dynamic. Thus companies with narrowly focused core competencies and limited capabilities are doomed. Collaborative ecosystems allow for more flexibility in fast-changing circumstances. Chinese ecosystems usually start out by co-developing a collaborative environment and creating network effects around the core business. Such collaborative ecosystems enable the core company to overcome capability gaps and discover new opportunities in adjacent industries that were previously out of reach. Companies in an ecosystem embrace ‘co-opetition’ – both competing and cooperating simultaneously to maximize their benefits.

Good artists copy…

Alipay has been growing and evolving as part of Alibaba ecosystem and its financial core. Launched in 2004 as an online payment and escrow service, Alipay may have at first appeared as China’s equivalent of PayPal. But the latest version of the Alipay mobile app (9.0, July 2015) shows it has grown from being ‘only’ a payment system into a one-stop portal for payment solutions.

Cutting out middlemen

By acting as an escrow agent, Alipay has cut out many of the middlemen that US merchants have to pay to (like banks and card networks). The apps are also free or near-free for users. As a result, the two giants – Alipay and WeChat – wield billions of dollars, which allowed them to add credit offerings, money-market funds that earn interest for users, and other pieces of the financial stack. Alipay, for example, offers credit services for consumers like Ant Credit Pay and Ant Cash Now. To give you a taste of the viability of this business model, consider this: Ant Financial Services Group (fka Alipay) is the most well-funded 2018 fintech startup, with circa $19.1B across 4 investments.

Airfox: the Robin Hood of emerging economies

MIT Technology Review gave this startup high acclaim among the transformative financial solutions for emerging markets. On a mission to take down financial barriers and provide opportunities to build wealth, Airfox aims to create an innovative payment app that serves the unbanked with reliable, egalitarian, and democratic access to capital and financial services. To power its revolutionary peer-to-peer microloans program, Airfox developed and released its own cryptocurrency, AirToken (symbol: AIR), an ERC-20 token issued on the Ethereum blockchain.

The app enables peer-to-peer payments and taking loans. For that, a user needs to initially make a deposit into their Airfox e-wallet (at 300,000 off-line locations, including ATMs and post offices) and make payments through the app (e.g., paying utility bills). Then, the app generates a credit score that makes a user eligible for a loan.

So how did they do it? Airfox utilises three technologies:

- Mobile. Users get full mobile payment experience.

- Machine learning. User smartphone data is used to create a credit score.

- Blockchain. Transactions go through blockchain where the loans are funded.

And from this starting point, the company aims to create financial instruments to put into blockchain and have anyone in the world finance their users.

In February 2018, the startup successfully brought thousands of unbanked and underbanked Brazilians access to mobile financing solutions. Airfox has already allowed nearly 15,000 users to engage freely in the financial economy. To significantly expand its footprint, Airfox signed a strategic partnership with a Brazilian retail giant and is currently preparing to extend the Airfox digital wallet to nearly 1,000 physical stores that serve 68% of Brazil’s population. It plans expansion to surrounding markets across Latin America.

How to get into P2P payment app development

When it comes to payment systems, security and standardization are on the forefront. It’s what led to the worldwide acceptance of card payments. With P2P payment solutions, preventing fraud and other issues is the only way to long-term success.

Foolproof design

The core challenge of all peer-to-peer systems is the overuse of shared resources in pursuit of self-interest. This is known as the ‘tragedy of the commons’.

To prevent storage and bandwidth overuse, decentralised peer-to-peer systems need to set up resource allocation and protection requirements. In particular, they need protection from 2 types of attacks: DoS and storage flooding. Design a P2P payment system to include certain accountability measures. By that we mean:

- Access restriction. This is realized by means of micropayments (the term can be misleading since it does not necessarily involve money exchange);

- Favorite user selection. Implement this via a user reputation. P2P apps have a user score impacting the access to resources and transaction enablement.

Regulation compliance

The fintech market is booming and we should keep in mind the regulations and complex laws that accompany all its processes. It’s still in the making, with some countries taking the lead and others lagging behind.

Asian sector has been at the forefront, issuing a number of FinTech regulations and standards.

The US is still fragmented and needs a more coherent approach in offering FinTech firms a legal framework which supports innovation and protects consumers. For example, the mobile payments industry has eight federal agencies with some oversight of finance and 50 states with their own rules. While in Canada, the new 2019 Bank Act will provide opportunities around open banking.

The UK fintech is regulated by the Financial Conduct Authority (FCA). The companies working on the European market know that alongside key standards such as ISO 20022, SEPA (Single Euro Payments Area), SWIFT 2017 and Fedwire, European Union (EU) is setting deadlines for adding the PSD2 (Revised Payment Service Directive) into national legislation to comprise the regulatory framework for payments. The EU’s GDPR aims to protect citizens’ personally identifiable information (PII), providing transparency around its use and giving people the right to restrict its use or request that it be deleted or ‘forgotten’ altogether.

Some disruptive technologies may run afoul of these standards and thus have to be implemented appropriately. There are FinTech regulatory sandboxes worldwide that allow you to test a business model and technology compliance, financial and operational impact.

P2P payment app user journey

Creating a mobile peer to peer payment app, you want to enable your users to:

- Transfer money into the app’s system. Pay-ins pull money from a user’s card (or bank, paypal, bitcoin account) into the system. The money actually lands in the app’s bank account. The computer system registers the amount in its database. This feature is normally monetized.

- Manage money in the system. You can freely transfer the money between the users in your system. It is instant and free since it only requires a change in the app’s database.

- Withdraw money from the system. Money in the system is pure digits. To make it physical and widely acceptable, you need to withdraw it into a bank account, load it into a prepaid debit card or put onto your paypal account. Pay-out incurs fees.

A peer-to-peer application does not usually directly interface with credit card and banking systems. It uses a financial services provider API.

P2P payment app features

Functionality is not the best area to experiment with. So focus on how to deliver quality UX to the features that stood a test of time:

- Unique ID/OTP – a user gets and verifies a unique ID or password each time a transaction is to take place. This is done for security reasons and users should be able to see all transaction details. Some P2P payment service providers ask for the OTP every time the app opens, to ensure a higher level of security. The fingerprints scan adds an extra layer of security to your app.

- User digital wallet – that’s the space for a user to keep the information on cards, discounts, special offers, in-app funds.

- Notification – the app marks the steps of payment initiation and completion and notifies the user of any activity in their account or wallet. Apart from that, users can get notifications of upcoming bill due dates, discounts, special offers, etc.

- Send/request money – this core feature enables users to actually send or request money. The 3S rule for this to be operational reads ‘Safety, Speed, and Simplicity’.

- Send a bill/Generate an invoice – users have to be able to scan and send bills that enable payments. They also need a feature that generate invoices of a transaction and stores them in the app.

- Transaction history – keeping data of all user payments in one place is possible with this feature.

- Transfer amount to bank account – a user may transfer the money received to their bank account via the app. This is a desirable feature to have in a money payment app.

- Messaging – sometimes a user needs to add details along with the transaction, in which case in-app chat is an easy and secure way to go. Chat capability is a nice-to-have feature in a P2P payment app. But the opposite holds true: a P2P payment capability may add great value and a competitive edge to your chat app.

Secure networks: Blockchain

P2P networks are faster and more reliable than centralized systems. They are also affordable and easy to maintain. But one thing that makes them inferior is security, which is at the same time of paramount importance in online payments. Both data transmission and storage are at a high risk of compromising. This is where Blockchain technology comes to the rescue and helps developers leverage the benefits of peer-to-peer networks.

Consider the potential of blockchain technology in securing cross-border payments – the weakest chain in P2P transactions. Banks, responsible for cross-border transactions, send user data (not money) by means of various technologies like SWIFT. Though time-tested, this method is:

- Costly. Every participating bank charges an interest, which can result in a pretty large sum. GDPR compliance makes the matters worse.

- Slow. The slow pace is partly explained by the ‘tired’ legacy technology: SWIFT and other solutions utilise Telex, and even telegraph.

- Non-secure. According to ThreatMetrix research, out of 1 billion of payment system bot attacks in 2018, two thirds were directed at Cross Border Payment Systems.

Though relatively new, Blockchain has received some proof of concept on a platform created by a Silicon Valley startup TBCASoft. The payment system is using the Rich Communication Services protocol (RCS), which is a communication protocol that aims at replacing SMS messages with a text-message system that is richer, provides phonebook polling (for service discovery), and transmits in-call multimedia. The protocol has been tested by the Japanese company SoftBank for P2P transactions between mobile operators. The system is taking off in 2019.

We at CodeTiburon favor AWS’ Blockchain service. It gives you a few options:

- Jump-start your project with Amazon Managed Blockchain;

- Scale it by using AWS Blockchain templates and Amazon ECS to give your microservices more flexibility.

Contact us to learn about other options.

Learn more about microservices: Microservices Architecture: to Build or Not to Build.

Wrapping-up

Stepping into the ocean of FinTech development is a great challenge but can be a game-changer. Only you can choose whether you want to turn your grain of wisdom into a pearl of a product or let it slide into the whirlpool of unfulfilled ambitions. Share your thoughts in the comments or give us a call.

How much does it cost to build a peer-to-peer payment app with CodeTiburon?

Good read and gives good points to consider should one want to venture.

Thanks, Bernard Oche. Appreciate your interest and feedback.

Excellent article. we are a young group willing t0 venture. I there any feasibility study that you can provide us so we know where we are heading. Thanks

Hello, Sam. Thank you for your interest! There’s no feasibility study available. But you can order one as part of pre-development business analysis.

Thanks for this wonderful article. Are there any resources that I can consider to inorder to build a successful mobile P2P app.

And to know the specific software requirements for such an app.

Hi.I am interested to know if you know any good developers that can create global money transfer app for sending and receiving like WorldRemit. I want to venture into this business. I have been trying to find a good developers. Do you have any recommendations.